How to Pay CPP and EI When You’re Self-Employed

If you run your own business, you have probably heard endless opinions about the smartest way to pay yourself. Some swear by a regular salary, while others insist dividends are the superior choice. Then there is the matter of the Canada Pension Plan (CPP), Employment Insurance (EI), and an entire alphabet soup of obligations that many people talk about, but very few take the time to explain in detail.

It is tempting to think these are small technicalities, yet the reality is that getting them wrong can quietly drain tens of thousands of dollars, or more, over the life of your business. The more you understand about how CPP and EI work when you are self-employed, the better prepared you will be to make decisions that protect both your cash flow and your long-term financial security.

Should You Opt-in to CPP and EI as a Self-Employed Business Owner?

When you are self-employed, every decision about how to pay yourself has a larger impact than most new entrepreneurs realize. It influences your immediate tax bill, your ability to save for retirement, and even how much flexibility you have if your income changes unexpectedly. Unlike a regular employee, you are not only the worker, but also the employer, which means that for CPP and EI, you are responsible for both sides of the contribution. That double obligation is something many people overlook until it is too late.

I see it often. Business owners assume the payroll rules they remember from past jobs still apply, but they fail to realize they are now paying twice the amount they once did.

How CPP Works for Self-Employed Business Owners

For a self-employed business owner, CPP contributions are structured in a way that guarantees you carry the full financial load. An employee only sees the deduction for their half on their pay stub, while the employer quietly pays the other half. When you are the employer, you are covering both portions.

For example, if you pay yourself $68,500 in salary, you will owe $7,735 in CPP. Every dollar comes directly from your pocket. The return you get for that money is not impressive. It is not a high-performing investment that compounds quickly over time. In fact, if you have the discipline to save and invest independently, you could almost certainly achieve a stronger return.

The One Distinct Advantage of CPP

The one distinct advantage of CPP is that it is exceptionally difficult to lose. If your business collapses or you are forced into bankruptcy, creditors cannot take it from you. That is not true for money held in your investment accounts or even certain retirement vehicles. For someone in a volatile or high-liability industry, this layer of protection can carry real value.

However, there is also an uncomfortable truth about CPP and self employment that people rarely discuss. The government can change the rules at any time. There is nothing preventing them from reducing benefits, restructuring the program, or even phasing it out entirely. At the moment, a significant portion of your contributions is going to support today’s retirees, many of whom paid in far less than you will. That imbalance is built into the system.

So, do I recommend CPP? Only if you know you will not save otherwise. If you need the forced savings mechanism, it is a safety net. But if you have the willpower and structure to build your own retirement fund, you may be better off limiting your CPP exposure. And under no circumstances should you continue paying salary beyond the CPP maximum of $68,500. Once you hit that ceiling, the extra contributions offer no additional benefit.

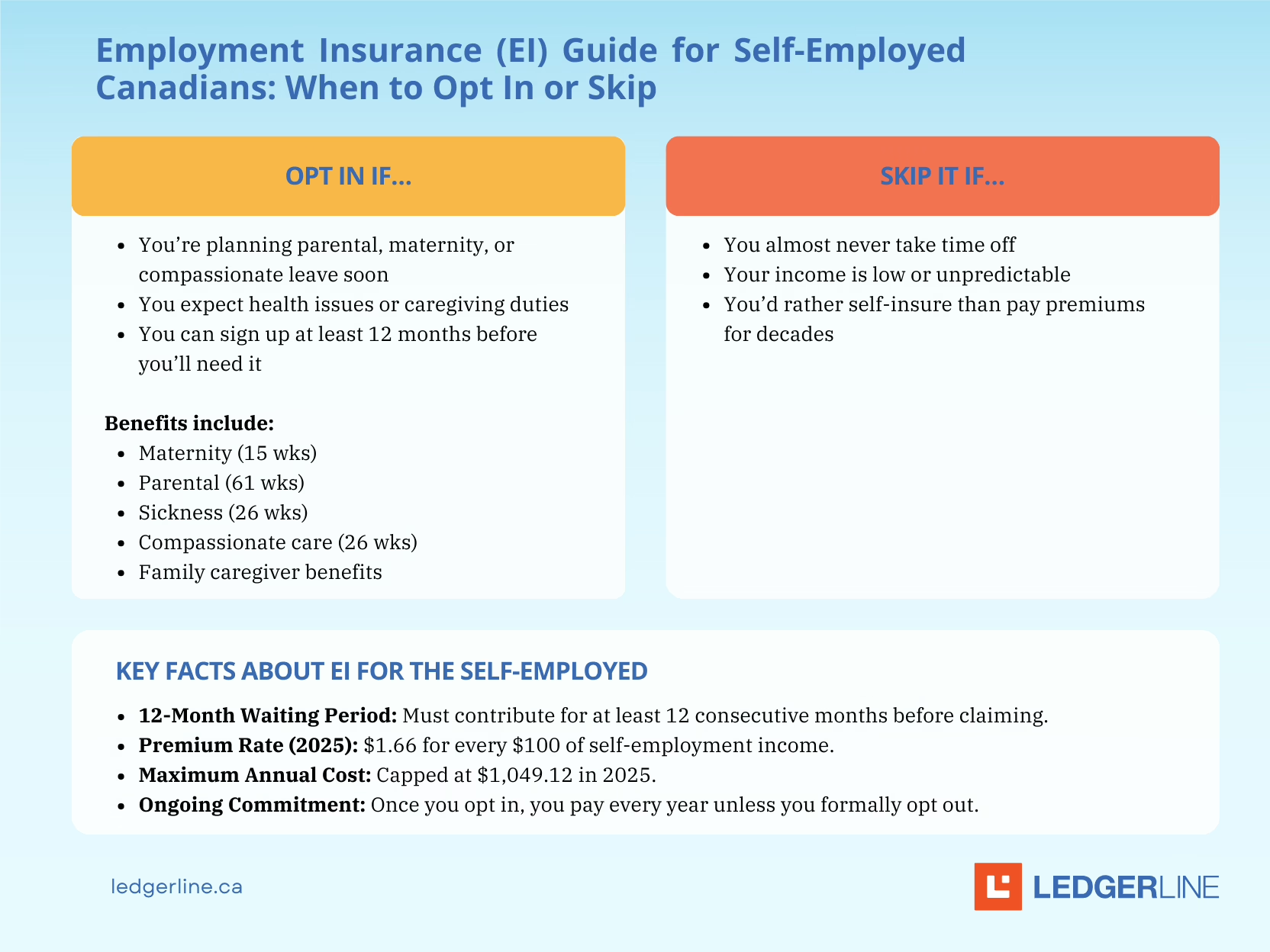

Is EI Worth Opting-in to?

In my experience, no. I have never had a self-employed client voluntarily opt-in to EI. I do not even bring it up unless there is a very specific and immediate reason for it. Once you opt-in, you are locked in for life. You will continue paying the premiums every year, and there is a strong possibility you will never collect the benefit.

The only time EI might make sense is when you have concrete plans to take parental leave or caregiver leave in the near future. Even then, the timing must be exact, because you need to opt-in well before a pregnancy or care need actually begins. If those plans fall through, you are stuck paying into a program you will not use.

I can only think of one client who dismissed EI entirely, and then wished they had it when their business shut down. My honest take? Business owners can face hardship, but most would rather be self-insured by setting money aside than to pay into EI for decades without return.

Salary vs. Dividends: Understanding What You Pay Into

The difference between salary and dividends is not just about the tax rate. A salary means you are paying into CPP, and possibly EI if you have opted in. It also creates RRSP contribution room, which is a powerful tax-planning tool that many overlook. Lenders also tend to view salary income more favorably if you ever need financing.

Dividends, on the other hand, bypass CPP and EI entirely, but they also bypass RRSP room. They may reduce your administrative burden, but they can also make you appear less stable to lenders.

The approach I recommend most often is a combination. If you want RRSP room and a limited level of CPP participation, take a salary up to $68,500. For all income above that, switch to dividends to avoid unnecessary payroll taxes. If you do not want to participate in CPP at all, pay yourself entirely in dividends — but only if you have a clear and consistent savings plan that actually gets funded.